I make no secret about the fact that I’m basically an adrenaline junkie. If given the opportunity, I’d travel around the world to ride every roller coaster there is. As it is, twice a year, Dad and I travel to the roller coaster capital of the world: Cedar Point. We drive 8 hours for the privilege of waiting in line, being tossed around and getting an adrenaline high (at least for me – Dad is just along for the ride). This past weekend was our last trip this year, and we go with good friends, which makes the experience even better – we have people to talk to in line 🙂

I love the ups and downs (and sideways) experiences that roller coasters give over and over again. But, I don’t really like my accounts to look like that.

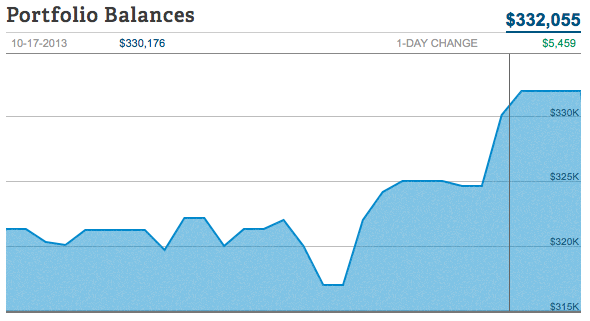

October’s portfolio balances

My checking account tends to look like that over time as money comes into and goes out of the account to pay for day to day things, and I accept that. But I don’t really like seeing the high hills and valleys in my retirement accounts. In technical terms, it’s called volatility – usually measured as a standard deviation from a mean. Thanks to the government shutdown and uncertainty, this is the view of our portfolio balances.

While it’s a roller coaster that I’d love to ride (that double dip there would really give some airtime), it’s not my favorite view of my balances.

Of course, daily viewing of your portfolio balances is discouraged for this very reason. I have enough mental constitution to not emotionally sell when things are down, but many people do not. If you’ve got a solid investment plan – whatever it is – stick with it, through the ups and downs. Only sell when your plan says to, not based on the market for that particular day.

Are you able to look at your balances daily (or even weekly) and stay the course with your strategy or do you sell when things look down?

Once I dial in my strategy I rarely check on my accounts. Maybe a couple times a year. I probably should tune into them a little more than I do, but so far it’s worked for me.

As long as you are doing what works for you. I like correlating news with market reaction, so it’s more of an academic curiosity for me than anything.

I’m guilty of checking in on my investments daily… probably not the best course of action for a passive long-term approach but it’s included in my Mint account, and I have an app on my phone so I’m constantly peeking in. So far, this hasn’t affected my strategy though, and I don’t plan on making any changes until my yearly scheduled rebalancing.

Thanks for stopping by! As long as it’s not affecting your strategy, I don’t see anything wrong with checking daily. Some people just can’t stomach the daily changes.

I check my investments about once a month (for the net worth post), and for better or worse have very little idea of how the market is doing until I do so at the end of the month. But I agree that the rollercoaster isn’t nearly as fun when it comes to our money.

As you go to Cedar Point, I wonder if you’ve ever been over to Kennywood in Pittsburgh. If you like wooden roller coasters, it’s a good place to check out.

I grew up on Kennywood (my grandparents lived in McKeesport)! My favorite there is Thunderbolt, and I can’t wait until Daughter Person is tall enough for the Jack Rabbit. We didn’t make it this summer, but if the weather isn’t too cold, we’ll take Daughter Person to see the Christmas lights there.

I only check in on investment accounts periodically since my strategy is long-term. Checking frequently would only stress me out!